November Market Report: Nimbus Performance & Outlook

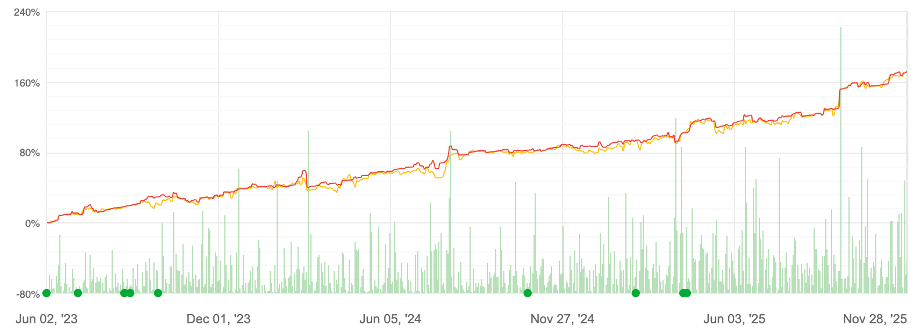

November offered little directional clarity. With limited U.S. data visibility, elevated macro uncertainty, and uneven price action across majors, conditions favored systems that could adapt quickly without overexposing to a single theme. Against that backdrop, Nimbus delivered an above-average +5.55% return for the month.

Execution & Efficiency

- Trades executed: 256

- Win rate: 73%

- Average holding period: ~20h 12m

- Profit Factor: 2.10 (total profits ≈ 2.1× total losses)

These metrics are consistent with Nimbus’s design: four fully independent, uncorrelated subsystems, reweighed by our NSGA-II genetic optimiser and ensemble ML filters to balance return, drawdown, and diversification in real time.

Drivers of Performance

- Top contributors: XAUUSD (long/short), USDJPY (long/short), EURUSD (long)

- Primary detractor: AUDUSD

Gold (XAUUSD) set the tone. Nimbus captured the pronounced two-way movement—benefiting early from strength tied to dovish Fed repricing, softer U.S. data, and renewed safe-haven demand—then pivoting tactically as sentiment moderated mid-month.

In USDJPY and EURUSD, the system’s momentum/mean-reversion blend allowed it to participate on both legs where appropriate, while correlation filters kept cross-exposure contained. AUDUSD detracted modestly; losses were controlled due to small sizing and the portfolio’s diversification constraints.

End-of-Month Positioning

By the final sessions of November, the largest aggregate exposure in Nimbus was USDCHF (long). The position reflected the subsystems’ consensus on carry and relative-rate dynamics alongside risk-aversion flows into the franc.

System Stewardship

We completed our standard month-end subsystem review and re-calibration—refreshing allocation weights, checking correlation drift, and validating execution assumptions. This process preserves Nimbus’s stability while maintaining responsiveness to evolving market regimes.

Outlook

Nimbus enters December with a balanced posture. Should policy rhetoric or data surprises accelerate trend formation, the optimiser can scale into momentum; if ranges persist, the portfolio’s mean-reversion and carry components remain prepared to harvest shorter-cycle opportunities—within the established drawdown controls.